8 Proven Methods for Sustainable Financial Growth

Financial growth is not a myth reserved only for the ultra-wealthy. People from all walks of life can build wealth. They can do this over time by focusing on key areas like budgeting, investing, and increasing income. Compound interest makes it possible. This guide explores 8 proven strategies. They are based on time-tested personal finance principles. They will put you on the path to financial stability and growth.

A single windfall rarely leads to lasting wealth. But, small, consistent, positive actions in how we spend, save, and invest our money can compound into huge dividends years later. Embracing sustainable finance trends, such as investing in socially responsible companies and green initiatives, can not only contribute to a better future but also potentially yield long-term financial gains. No matter your finances, using a few research-backed methods in this article can free you from real or self-imposed limits. They hold you back from reaching your full potential.

The time is now to take control of your financial life trajectory. By the end, you’ll have the insights and tools to start writing your own wealth-building story. It’ll be fueled by ambition, smart choices, and conscious money habits. It all starts with turning that first page by expanding your financial knowledge into action.

I. Strategic Investment Planning: Laying the Groundwork

Investing your money wisely is essential. It ensures it works well for your long-term goals. The right investment strategies can set you firmly on the path towards sustainable financial growth.

Diversify Across Asset Classes

Keeping all your money in just stocks, bonds, or even a single company poses extreme risks. Diversifying across different asset classes reduces risk through exposure to varied economic conditions.

While stocks offer growth potential, their prices fluctuate wildly. Bonds provide steady interest income but limited upside. Real estate can generate rental income while also appreciating over decades. And cash equivalents like CDs or money market funds offer stability.

Decide the right mix for these core asset classes. Base it on your risk tolerance and investment timeline. Use historical return data.

Diversify Across Market Sectors

The economy contains 11 key sectors, from technology to healthcare to consumer staples. Different sectors perform differently in various business cycles.

Diversify stock investments across sectors to smooth out volatility. Overweight sectors with strong tailwinds while underweighting struggling ones.

For example, the energy sector surged in 2022 amid high oil prices. But alternative energy stocks plunged. Blend both for diversification.

Diversify Across Company Sizes

Both large established corporations and small upstart companies have pros and cons for investors.

Large caps are historically less volatile with steady dividends but lower growth potential. Small caps exhibit far higher volatility but with greater upside when they succeed.

Holding both across an index fund or portfolio balances out these factors.

Diversify Across Global Regions

Economic and political conditions vary significantly across countries and geographic areas.

Diversifying investments across global regions helps insulate from localized risk.

For example, investing solely in Chinese stocks exposes one to intense volatility whenever Chinese policies or growth prospects shift.

II. Debt Management and Reduction: Lightening the Load

High monthly debt payments constrain cash flow available for investing towards financial growth. Implementing proven debt management strategies alleviates this burden long-term by freeing up capital, thereby providing more resources for investment.

Many New York residents struggle with overwhelming high interest debts that become difficult to manage. These debts can include credit cards, personal loans, medical bills, and other financial obligations. As debts grow, monthly payments rise, putting great financial strain on individuals and families. This leads many New Yorkers to seek help with their debt problems.

Specialized New York debt relief programs are available to help negotiate, consolidate, and reduce monthly payments to affordable levels for residents facing unmanageable debts.

Employ the Debt Snowflake Method

The debt snowflake method combines the debt snowball and avalanche approaches by paying extra towards your highest interest debts while still paying minimums on all accounts. Specifically:

- Make minimum payments across all debts

- Put any extra funds towards higher interest debts first

- Once a debt is cleared, roll its minimum payment to the next highest interest debt

This keeps motivation high by eliminating debts quickly while optimizing interest cost reductions.

Refinance Debt Strategically

Replacing high-interest loans with lower rate alternatives accelerates repayment, saving money long-term.

Run the numbers to confirm refinancing indeed lowers lifetime interest expenses after accounting for fees. Refinance when the numbers decisively warrant doing so.

Additionally, shifting credit card balances to a single 0% APR card saves substantially on interest payments for 12-18 months. This temporary 0% window assists rapid payoff.

Leverage Balance Transfer Credit Cards

Balance transfer cards offer 0% APR on transferred debt for over a year, enabling natural paydown without accumulating further interest.

This works best for smaller consumer debt amounts rather than mortgages or student loans. Pay transfers off completely within the 0% duration to maximize savings.

III. Income Diversification: Expanding and Protecting Revenue Streams

Relying solely on a single income source is highly risky. Job loss would simultaneously eliminate your income flow.

Income diversification improves resilience against disruption by creating multiple cash inflow streams, including passive income.

Generate Multiple Passive Income Channels

Passive income requires effort upfront but then earns money with minimal ongoing time investment, through avenues like:

- Rental real estate

- Dividend stocks/index funds

- Royalties from creative work or patents

- Affiliate marketing programs

- Selling informational products like eBooks or courses

- Creative assets that generate royalties like songs or apps

- Build several passive channels to create diversified cashflow for stability through changing economic conditions.

Develop Multiple Side Hustles

Side hustles enable earning extra income from a hobby, passion or skill during your free time. Popular options include:

- Freelancing in areas like software development, writing, design etc.

- Starting a YouTube channel that monetizes with ads

- Buying products wholesale and reselling for profit

- Walking dogs, house sitting, running errands for others

- Making and selling crafts, jewelry, woodwork and more

Side hustles not only boost current income, but also provide alternate employment options if ever needed.

IV. Budget Optimization: Maximizing Your Money

Budgeting is essential for sustainable financial growth. Meticulously tracking expenses and savings frees up more capital for wealth-building investments.

Adopt a Zero-Based Budget

With a zero-based budget, every dollar earned is budgeted for an intended purpose. Unbudgeted surplus cash can unconsciously get frittered away on frivolous expenses. Assigning each dollar a purpose preemptively puts savings and investing first before spending.

Popular zero-based budget methods include the 50/30/20 budget, bucket budgeting, and reverse budgeting. Zero-based budgeting apps make this approach easy to implement.

According to surveys, zero-based budget users save 20-40% more than those without a formal budget.

Utilize Expense Tracking Apps

Apps like Mint, Personal Capital, and You Need a Budget provide intuitive interfaces for tracking all your expenses. They generate helpful analytics on spending patterns and even provide budgeting advice.

Synchronizing all financial accounts into such an app makes money oversight easy. The awareness naturally leads to more mindful purchasing choices.

84% of app users say expense trackers help them better manage finances. Leverage technology to optimize your budget.

V. Long-term Financial Planning: Mapping the Route Ahead

Reaching long-term financial goals requires prudent planning around investments, asset allocation, retirement needs, and risk management.

Set S.M.A.R.T Financial Goals

Applying the S.M.A.R.T framework when setting financial goals boosts the likelihood of achieving them:

- Specific – Clearly defined objectives

- Measurable – Quantifiable targets to track

- Achievable – Challenging but viable given your situation

- Relevant – Aligns with your values and priorities

- Time-bound – Defined deadlines

Review and adjust goals periodically as life situations evolve.

Build an Emergency Fund

A liquid emergency fund containing 3-6 months’ worth of living expenses is vital for surviving income disruptions. It prevents acquiring further high-interest debt due to unexpected crises.

Automate emergency fund contributions to ensure consistent buildup. Review fund size annually and after major life events. An emergency buffer brings tremendous financial and mental stability.

According to the Federal Reserve, 40% of Americans cannot cover a $400 emergency expense. Don’t be part of that statistic.

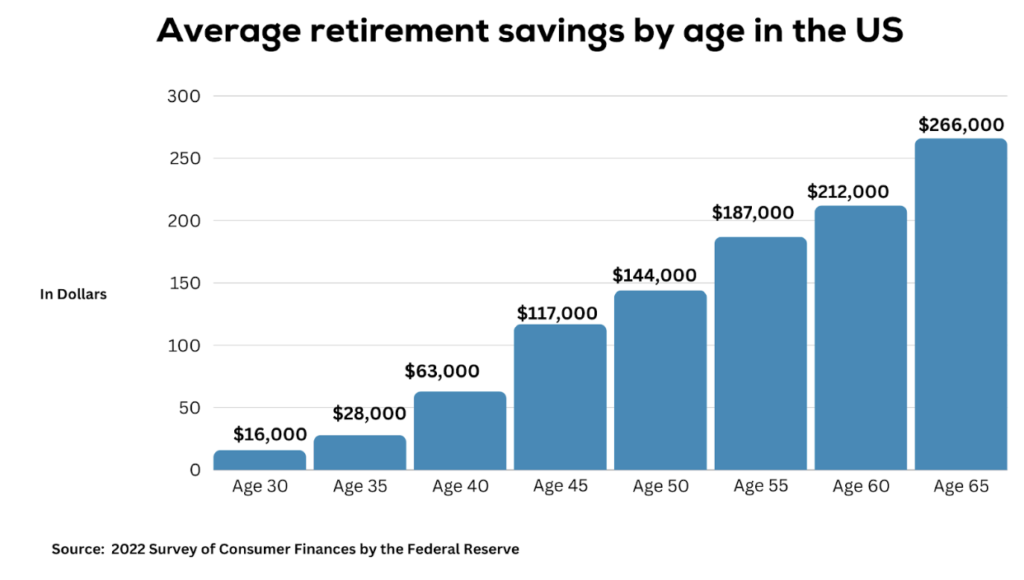

Plan Early for Retirement

Retirement funds grow exponentially as the earlier contributions begin due to compound interest. Someone who invests $5,000 annually from ages 20-30 and nothing more will still end up with substantially more retirement savings than another person investing $5,000 annually from ages 40-65.

Start saving for retirement as early as possible. Consistent contributions in a tax-advantaged account with an appropriate asset allocation set the stage for sustainable long-term growth.

VI. Sustainable Spending Habits: Aligning Consumption with Goals

Mindless and reactionary spending is easy with online shopping and instant digital payments. Consciously developing sustainable spending habits aligns daily purchases with your financial growth plans.

Adopt Conscious Consumption Habits

Strive to only purchase items you genuinely need and will use long-term. Prioritizing purposeful purchases on quality goods you value highly optimizes the utility derived from your spending budget.

Before buying discretionary items, ask yourself:

- Will this purchase add value to my life?

- How often will I foreseeably use this item?

- Are there alternatives that meet my needs as effectively for lower cost?

Carefully consider necessity, utility, longevity, and alternate options before mindlessly spending on fleeting wants.

Avoid Lifestyle Inflation Pitfalls

It’s tempting to increase spending as income rises in pursuit of social status. Yet lifestyle inflation erodes potential savings and investments to pay for unsustainable consumption.

Be cognizant if lifestyle spending starts notably outpacing earnings growth. Reign in overly lavish purchases that do little to enhance financial sustainability. Savvy spending habits, not flashy signals of wealth, enable genuine growth.

VII. Continual Financial Education & Literacy

Ongoing learning is crucial for making informed financial decisions aligned with your growth objectives as economic conditions evolve.

Commit to Continuous Financial Learning

The most successful investors and entrepreneurs voraciously self-educate throughout their lifetime. They read books, publications, listen to money podcasts, and take courses to constantly expand their financial knowledge.

While formal education has a curriculum, self-education never ends. Make reading and learning about financial principles, products, and best practices a lifelong habit. This fuels sustainable growth.

According to studies, financial literacy positively correlates with indicators like household net worth and participating in the stock market. Never stop striving to expand your money wisdom.

VIII. Leverage Fintech to Unlock Growth Potential

Financial technology innovations provide sophisticated tools for optimizing everything from budgeting to investing. Embracing fintech establishes scalable systems for sustaining wealth accumulation.

Implement Automated Investing & Savings

Platforms like Betterment, Acorns, and Robinhood enable automatically depositing funds into managed investment accounts on schedule. This hands-off discipline removes human interference that often hinders portfolio growth.

90% of Betterment users say the platform helps them manage finances and save more successfully. Set up recurring transfers into investment accounts to put savings and compound growth on autopilot.

Explore Cryptocurrency Investing

Cryptocurrencies like Bitcoin and Ethereum constitute an entirely new digital asset class with intriguing properties. Savvy investors have achieved outsized returns from the immense growth cryptocurrencies have experienced recently.

Over 190 million people worldwide now own cryptocurrencies. While incorporating some crypto exposure can boost portfolio returns, only invest an amount you can afford to lose given the volatility.

FAQs

What are some first steps to get started with financial growth?

The first steps involve fully analyzing your finances. This includes your income, expenses, assets, and debts. You should also compare to peers using net worth calculators. Outline short and long term personal finance goals. Then make milestones for spending, saving, and investing. Also, for cutting debt. These should match the growth goals and risk level found in assessments.

What percentage of my income should I save and invest?

Ideally, 10-20% of income should go into savings and investments. But the right percentage depends on the context. Those with high-interest debt may need to put more temporary cash towards repaying debt. They should do this before heavily investing. Young investors should target 20% or more to maximize time and compound interest. Include employer retirement contributions and match in assessing target savings rate.

How do I select the right investments for my goals?

Outline your risk tolerance and time horizon. Then study the past returns of assets like stocks, bonds, and real estate. Use this to decide how to divide your investments to balance risk and return for your situation. Diversify across sectors, geographies, market caps, etc. utilizing low-cost index funds. Frequently reassess portfolio exposures as personal context and market conditions evolve. Enlist a fee-based financial advisor if needing personalized guidance.

What should I do with a financial windfall?

First, set aside an emergency fund. It should cover several months of living expenses. Only after that, use windfall money for other goals. Next, pay down any high-interest debts. Finally, invest the rest in passive index funds. The funds are focused on stocks and bonds. Choose ones matched to your timeline and risk appetite. Avoid speculating on individual risky assets. Unlock a windfall’s power through smart savings and debt cuts. Also, use compounding with diverse, passive investments.

Conclusion

Using just a few of the strategies for sustainable financial growth outlined here can lead to huge wealth. The strategies are about budgeting, investing, paying off debt, and diversifying income. This can happen over months and years through consistency and smart choices. Investing seems complex. But, the basics of personal finance are simple. They are to spend smartly, save diligently, and invest your working money wisely. Small differences in daily and weekly routines snowball in a revolutionary way.

The journey needs patience, hard work, sacrifice, and ongoing financial smarts. But, committing to lasting wealth creation pays huge dividends that money cannot count. These include a sense of financial security and control over life. They also include pride in delayed gratification and confidence to pursue passion projects. Also, it means a more meaningful legacy to leave behind for causes and people you care about. Stay focused on the short-term process, but keep the big-picture impact in mind. Invest in financial knowledge and in yourself. Believe in the math and principles underlying these proven financial growth strategies. Your future self across the compounded years will thank the wiser you of today.